Building a Subprime Department at Your Dealership

Autocarleads | Updated April 2026 | 8 min read

Most dealerships that serve subprime buyers don’t have a subprime department.

They have a standard finance operation that occasionally handles a challenging credit application and hopes for the best.

That’s a different thing from a purpose-built subprime operation and the results reflect that difference consistently.

Building a dedicated subprime department at your dealership isn’t just about adding a desk and calling someone the subprime manager. It’s about creating a specific infrastructure, lender relationships, deal structure process, lead pipeline, and team capability that serves this buyer profile consistently rather than occasionally.

This article covers what that infrastructure actually looks like and how to build it without losing ground on your standard finance operation in the process.

Why a Dedicated Operation Outperforms an Ad-Hoc Approach

The difference between a dedicated subprime operation and a standard finance desk that occasionally works challenged credit comes down to one thing. Consistency.

Subprime deals require specific lender knowledge, specific deal structure discipline, and a specific buyer conversation. When those things are handled by a finance manager whose primary focus is standard credit deals and who picks up a subprime application occasionally, the results are inconsistent.

Lender routing decisions get made based on gut feel rather than criteria. Deal structures get submitted before being checked against payment-to-income thresholds. Buyer conversations get handled with a standard approach that doesn’t account for the different emotional context of a subprime buyer. Approvals happen when everything aligns by chance. Declines happen more often than they should.

A dedicated operation runs the same checklist on every deal. The same lender routing logic. The same deal structure verification before submission. The same buyer conversation calibrated for this specific profile. The results are predictable rather than variable because the process is consistent rather than improvised.

Step 1: Decide What Kind of Subprime Operation You’re Building

Before you hire anyone or call a new lender, get clear on what you’re actually trying to build.

There are two meaningfully different models for dealership subprime operations.

The integrated model

Subprime buyers are handled within the existing dealership structure by finance managers who are trained and equipped for both standard and challenged credit applications. The same team handles both. The workflow and lender routing are designed to accommodate both buyer profiles.

This model works well for dealerships where subprime volume is significant but not dominant. It doesn’t require separate staffing and it allows finance managers to develop capability across the full credit spectrum rather than specializing in one tier.

The dedicated model

A separate team, sometimes a separate physical space, handles subprime applications exclusively. Standard credit goes one direction. Challenged credit goes another.

This model works well for dealerships where subprime is a core business focus rather than a supplement to standard financing. It allows deeper specialization, stronger lender relationships within the subprime tier, and a buyer experience that’s consistently calibrated for this profile.

Most dealerships starting out in subprime begin with the integrated model and move toward the dedicated model as volume justifies the additional structure. Knowing which you’re building toward helps you make the right infrastructure and staffing decisions from the start.

Step 2: Build the Right Lender Relationships

This is the foundation of everything else. A subprime department without the right lender relationships is a team with no tools.

You need at minimum two or three strong relationships with specialist subprime lenders whose credit tier appetite, vehicle requirements, and deal structure criteria you know in detail. Not in general terms. In specific terms that tell you exactly how to route an application before you submit it.

For each lender relationship, know the following.

Minimum and maximum credit score for their primary subprime product. Whether they have separate tiers within the subprime range and what those look like. Minimum down payment requirements at different score levels. Maximum vehicle age and mileage they’ll finance. Maximum LTV they’ll work to. Payment-to-income ratio threshold. States they operate in. How they handle income verification for self-employed buyers.

That information should live in a reference document your finance team can access during every deal. Routing decisions made from memory rather than documented criteria produce routing errors that cost approvals.

Beyond the two or three core relationships, having a buy here pay here option as a safety net for buyers who don’t fit any external lender’s criteria keeps the door open for deals that would otherwise walk out.

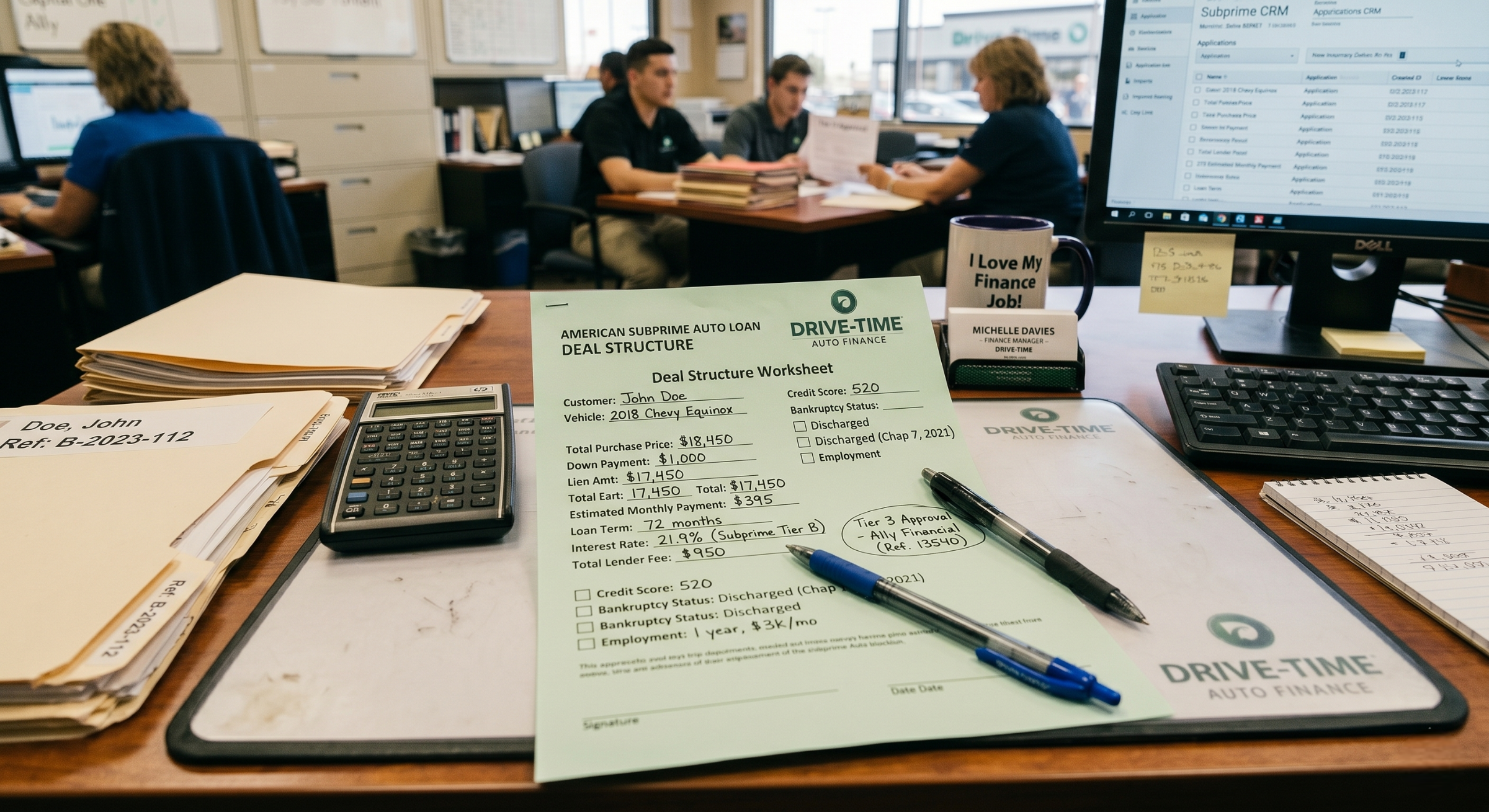

Step 3: Define Your Deal Structure Process

Every subprime application that goes to a lender should be structured before it’s submitted, not after.

Build a simple deal structure worksheet that your finance team completes before every submission. It should capture the following.

Buyer’s verified gross monthly income. Proposed monthly payment. Payment-to-income ratio calculated from those two numbers. Vehicle purchase price and book value. Proposed loan amount and calculated LTV. Buyer’s available down payment. Lender being considered for submission and their specific thresholds.

If the numbers don’t fit the lender’s criteria before you submit, adjust the structure. Increase the down payment, reduce the vehicle price, extend the term within the lender’s limits, or identify a different lender whose criteria the current structure fits better.

This process takes 10 minutes and prevents most structural declines. Structural declines are the ones that cost the most because they add hard inquiries without producing approvals and they damage the relationship with buyers who interpret a decline as a verdict rather than a routing error.

Step 4: Staff and Train Specifically for Subprime

Whether you’re building an integrated or dedicated model, the people handling subprime applications need specific training that goes beyond standard finance manager preparation.

What subprime-specific training covers

Credit tier knowledge. Understanding what the different score ranges mean for lender options, deal structure requirements, and rate expectations is foundational. Finance managers who treat subprime as a monolithic category rather than a spectrum make routing errors consistently.

Deal structure mechanics. Payment-to-income ratio, LTV calculation, down payment impact, and term selection all require specific knowledge to apply correctly. Running through these calculations manually on sample deals during training builds the instinct to apply them automatically in real situations.

The buyer conversation. A subprime buyer needs a different opening, a different rate conversation, and a different timeline management than a standard credit buyer. Training on the specific language and approach that works with this buyer profile is worth doing deliberately rather than leaving it to individual finance managers to figure out through trial and error.

Lender routing. Your finance team should know the specific criteria of each lender relationship well enough to route without always needing to reference the documentation. That level of familiarity comes from repeated application over time but it starts with deliberate training on what each lender’s appetite looks like.

What ongoing development looks like

Monthly review of subprime performance by finance manager. Which lenders are producing approvals. What deal structures are working. Where the declines are coming from and what patterns they reveal. This review process is how you identify training gaps before they become persistent performance problems.

Lender relationship updates. Lender criteria shift periodically. What a lender would approve 12 months ago may not match what they approve today. Building regular check-ins with your lender contacts into the operation keeps your routing knowledge current.

Step 5: Build a Consistent Lead Pipeline

A subprime department without a consistent lead pipeline is an operation that runs when subprime buyers happen to walk in and goes quiet when they don’t. That’s not a department. That’s an occasional capability.

Purchased subprime leads give the operation a consistent pipeline independent of walk-in traffic. They let you staff appropriately, train consistently, and build lender relationships around predictable volume rather than sporadic demand.

The quality of the leads matters more in subprime than in standard credit because the deal structure requirements are more specific. A subprime lead that’s outside your geographic service area or misclassified as subprime when the buyer is actually near prime creates routing confusion and wasted effort. Leads with verified credit range data and accurate geographic targeting give your team the right starting information before the first call.

Building a reliable subprime lead pipeline through a quality provider is what turns a subprime capability into a subprime operation. The infrastructure you build around the leads is what converts them. But consistent volume is what keeps that infrastructure active and improving.

Real-time delivery into your CRM matters in this segment. Subprime buyers who submit a lead and don’t hear from anyone quickly sometimes interpret the silence as another rejection. Reaching them within five minutes of submission catches them at the peak of their engagement with the process and before that interpretation has time to set in.

Step 6: Create a Subprime-Specific Follow-Up Process

Standard lead follow-up sequences need modification for subprime buyers.

More touches are typically needed before a subprime buyer engages in a productive conversation. The uncertainty about whether approval is possible at all can make buyers hesitant to respond until they feel confident the outreach is genuinely trying to help rather than going through motions.

The messaging between touches should reflect where the buyer likely is mentally rather than just following a generic check-in script. An opener that acknowledges the credit situation directly and frames it as something the dealership works with regularly creates a different pull than a standard vehicle-focused opening.

Follow-up timelines for unresponsive subprime leads should extend longer than for standard credit leads. A buyer who submits a lead, doesn’t respond for a week, and then engages on day nine is a real pattern in this market. Don’t move leads to inactive status too quickly.

Step 7: Build the Right Inventory Mix

A subprime operation needs inventory that subprime lenders will finance.

Most specialist subprime lenders have vehicle restrictions around age and mileage. Vehicles over 10 years old or above 100,000 to 120,000 miles create LTV problems and lender coverage gaps regardless of how well the rest of the deal is structured.

Having a meaningful selection of reliable used vehicles in the $8,000 to $20,000 range that fit within typical subprime lender criteria gives your finance team something to work with for the majority of subprime buyers. A subprime department that regularly has to turn buyers away because the available inventory doesn’t fit the financing reality is leaving deals on the table that a better-stocked lot would close.

New vehicle inventory can also serve near-prime and upper-subprime buyers when manufacturer financing programs extend into those credit tiers. Knowing which of your captive financing partners have products that reach into the subprime range and keeping relevant new inventory available for those approvals adds another deal pathway.

Step 8: Track Performance Metrics Specifically for Subprime

Running a subprime operation without specific performance tracking is running it blind.

The metrics that matter are the same as any finance operation but they need to be tracked specifically for subprime rather than blended with your overall numbers. Blended numbers hide the performance of the subprime operation specifically and make it impossible to identify where the process needs improvement.

Track the following monthly for your subprime operation specifically.

Lead volume by source and credit tier. Contact rate on subprime leads. First-attempt approval rate by lender. Overall subprime closing rate. Cost per closed subprime deal by lead source. Average gross profit per subprime deal. Refinance and repeat purchase rate from subprime customers over time.

The last metric on that list is worth particular attention. Subprime buyers who have a good experience and improve their credit over time represent a compounding return on the relationship. Tracking how many of your subprime customers come back, refer others, or refinance through you tells you the real long-term value of the operation beyond the initial deal.

Tracking subprime department performance by the right metrics is what turns the operation from a cost center into a measurable business unit with a clear contribution to overall dealership profitability.

Step 9: Compliance From the Start

Subprime auto financing has attracted regulatory attention and building compliance into the operation from the beginning is significantly easier than retrofitting it after a complaint or enforcement action.

The key compliance areas for a subprime department include fair lending practices under the Equal Credit Opportunity Act, accurate disclosure of rates and terms, consistent application of credit criteria without discriminatory patterns, and the specific state-level regulations around fee disclosure and dealer practices in your market.

Working with a compliance consultant or attorney to review your subprime operation’s processes before you scale is an investment that prevents far more expensive problems down the road. Lenders with strong compliance records also tend to have more lender options available to them because specialist subprime lenders evaluate their dealer partners’ compliance posture as part of the relationship.

The Customer Experience Standard

A subprime department that processes applications efficiently but treats buyers poorly is building a short-term business without a long-term foundation.

Subprime buyers who have a positive experience, who feel respected rather than tolerated, who receive honest information about rate and terms and a genuine effort to find them the best available option, come back. They refer people. They represent the referral engine and repeat business that make a subprime operation genuinely profitable rather than just occasionally productive.

Setting an explicit customer experience standard for the subprime department and holding the team to it is worth doing as deliberately as you set the deal structure process. The standard should include how the rate conversation is handled, how declines are communicated and what happens next, and how follow-up after the sale is structured.

What the Operation Looks Like When It’s Working

When a subprime department is functioning well, a few things become visible.

The finance team routes applications to the right lender on the first attempt more often than not. Structural declines become rare because the worksheet catches the problems before submission. Buyers who come in uncertain about whether approval is possible leave with a clear answer and in most cases with a realistic path forward.

The lead pipeline is consistent enough that the team is always working and always improving their process. Performance metrics are tracked monthly and reviewed with the team so improvements are deliberate rather than accidental.

And the customer experience is good enough that a meaningful percentage of subprime deals produce a second deal, a referral, or a refinancing relationship down the road.

That’s not an aspirational standard. It’s what a well-built subprime operation actually produces.

The Bottom Line

Building a subprime department is a genuine operational investment. It requires lender relationships, trained staff, a structured deal process, a consistent lead pipeline, the right inventory, specific performance tracking, and a compliance foundation.

What it produces is access to a large, underserved buyer segment with real loyalty potential and a consistent revenue stream that most competitors have decided isn’t worth the effort to build.

The dealerships that build this capability properly and run it consistently find that the investment pays back quickly and compounds over time as the customer base grows and the team gets sharper with experience.

How Autocarleads Supports Subprime Department Operations

Every subprime lead that comes through Autocarleads is intent-verified, contact-validated, and matched to your geographic market. Credit range classification is based on verified data so your team knows exactly what tier they’re working with from the first call.

Real-time delivery into your CRM means your team reaches buyers at the peak of their engagement with the process. Filtering options let you dial in the specific credit range and geographic area that matches your lender relationships and service area.

See what subprime lead options are available in your market and how the matching works.

Frequently Asked Questions

How much volume do I need before a dedicated subprime department makes sense?

There’s no universal threshold but a useful rule of thumb is that if subprime applications represent more than 20 to 25 percent of your finance volume and you’re not closing them at a rate that reflects their potential, a dedicated operation is likely worth building. Below that volume, the integrated model typically makes more sense. The decision should be driven by the gap between your current subprime performance and what a well-run operation would produce rather than by volume alone.

How many lender relationships do I need to start a subprime operation?

Two strong specialist subprime lender relationships give you meaningful routing flexibility across most of the subprime range. Three is better because it covers more of the spectrum and provides redundancy when one lender tightens its criteria or changes its vehicle requirements. Starting with one relationship and hoping it covers everything is the most common setup error in new subprime operations.

Should subprime leads go to a dedicated BDC or directly to finance managers?

It depends on your volume and team structure. A dedicated BDC handling first contact and qualification for subprime leads is effective when volume justifies the staffing. In lower-volume operations, finance managers handling first contact directly builds the buyer relationship from the start and avoids a handoff that can disrupt the continuity that matters more in subprime than in standard credit. The key is that whoever makes first contact is trained specifically for the subprime buyer conversation.

How do we handle the transition from a standard finance operation to an integrated subprime capability?

Start with lender relationships and training before you scale lead volume. A finance team that doesn’t know how to route or structure subprime deals correctly will produce poor results from good leads. Get the infrastructure right first, bring in a manageable initial lead volume to build the team’s experience, track the results carefully, and scale from there as the process proves itself.

What's the realistic timeline to build a functioning subprime department from scratch?

A basic functional capability, meaning trained staff, two or three lender relationships, and a structured deal process, can be in place within 60 to 90 days for a dealership that prioritizes it. A consistently performing operation with tracked metrics, an optimized lead pipeline, and a team that routes and structures confidently takes 6 to 12 months of operational experience on top of that foundation. The infrastructure takes weeks to build. The expertise takes months to develop.