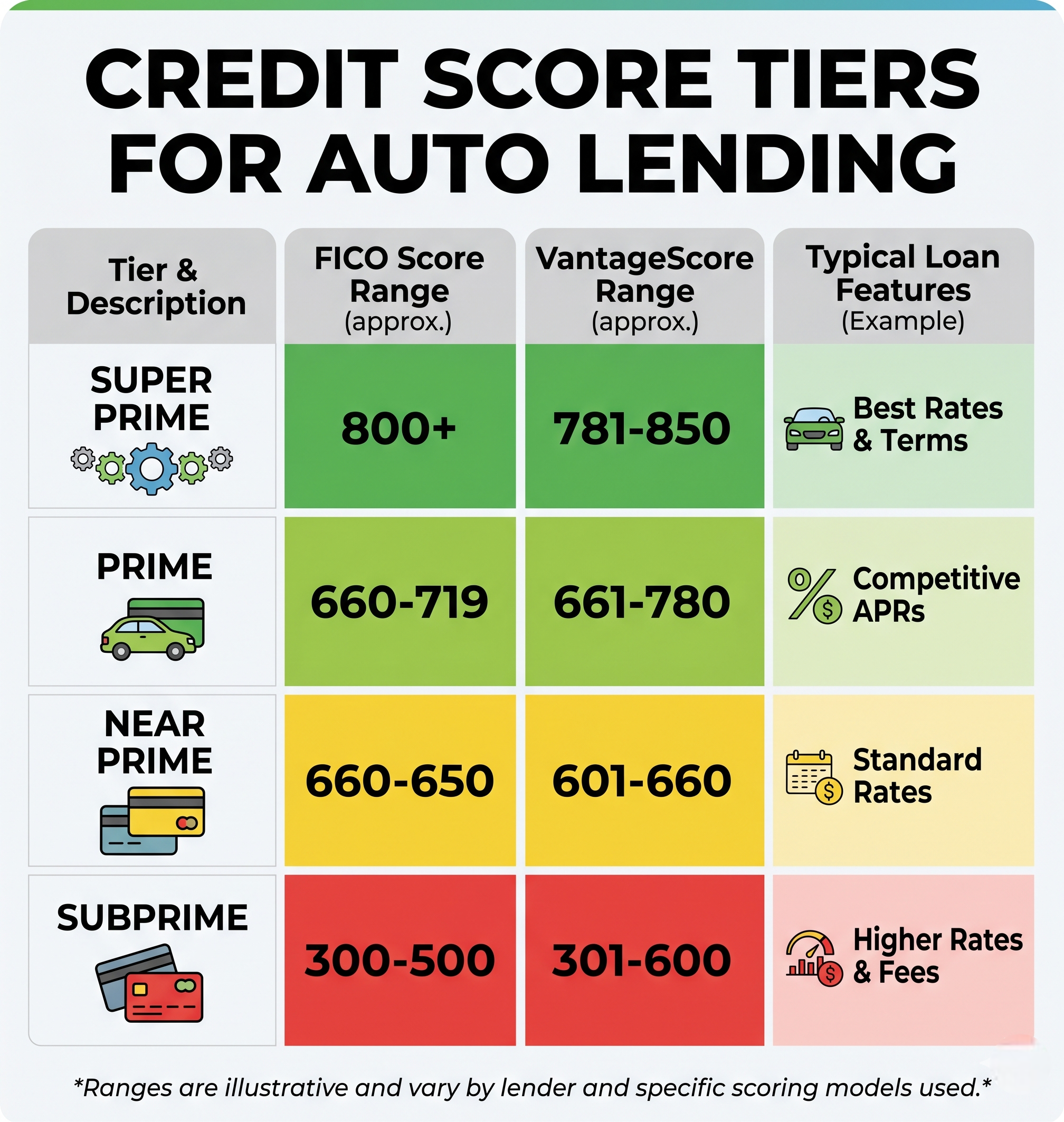

The Standard Credit Tiers in Auto Lending

The auto lending industry uses a broadly consistent set of credit tiers though the exact boundaries vary slightly between lenders. Here’s how the market generally defines them.

Super Prime: 781 and Above

The top tier. Buyers in this range represent the lowest risk profile in the market. Lenders compete for these applications and the rates offered reflect that competition.

For dealers, super prime buyers are straightforward to finance. The priority is speed and rate competitiveness. Getting them approved quickly at the best available rate is what matters. Captive finance companies and national banks are typically your first call here.

Prime: 661 to 780

Solid credit with a strong track record. Buyers in this range qualify for most standard auto loan products at competitive rates. The approval process is generally smooth and the lender pool is wide.

Rates in this tier are meaningfully lower than subprime, which keeps monthly payments manageable even at higher vehicle price points. Most of your standard dealership volume likely falls somewhere in this range.

Near Prime: 601 to 660

This is the transition zone between prime and subprime and it’s where routing decisions start to matter more.

Near prime buyers may qualify for standard financing through some lenders but not others. Some captive finance companies have products that reach into the near prime range. Others cut off at 660 or 680. Knowing your specific lenders’ thresholds tells you whether a near prime buyer goes to a standard channel or a specialist one.

Rates in this tier are higher than prime but not dramatically so for buyers toward the upper end of the range. Deal structure matters more here than at higher tiers because the margin between an approval and a decline is thinner.

Subprime: 501 to 600

This is the core subprime range. Traditional banks and most credit unions are not useful channels for buyers in this tier. Independent finance companies that specialize in challenged credit are your primary lender options.

Rates in this tier are significantly higher than prime. Down payments are typically required. The underwriting process is more detailed and deal structure carries more weight in determining whether an application gets approved.

Buyers in this range often know their credit is challenged. They’ve usually encountered the reality of their credit score in a previous financing attempt or through checking it themselves. The conversation works better when it starts from that shared understanding rather than dancing around it.

Deep Subprime: 500 and Below

The most restricted tier in terms of lender options. Most independent finance companies have floors around 500 or slightly above. Below that threshold, buy here pay here and a small number of deep subprime specialist lenders are typically the only realistic channels.

Approval in this tier almost always requires a meaningful down payment, a vehicle within a specific price and age range, and verified stable income. Deal structure is not just important here. It’s often the difference between making the deal happen and not.

Buyers in this range sometimes have circumstances behind their score that explain it, recent bankruptcy discharge, medical debt, a specific period of financial difficulty, that provide context worth understanding before you structure the deal. Income stability and employment history carry more weight in deep subprime underwriting than in any other tier.