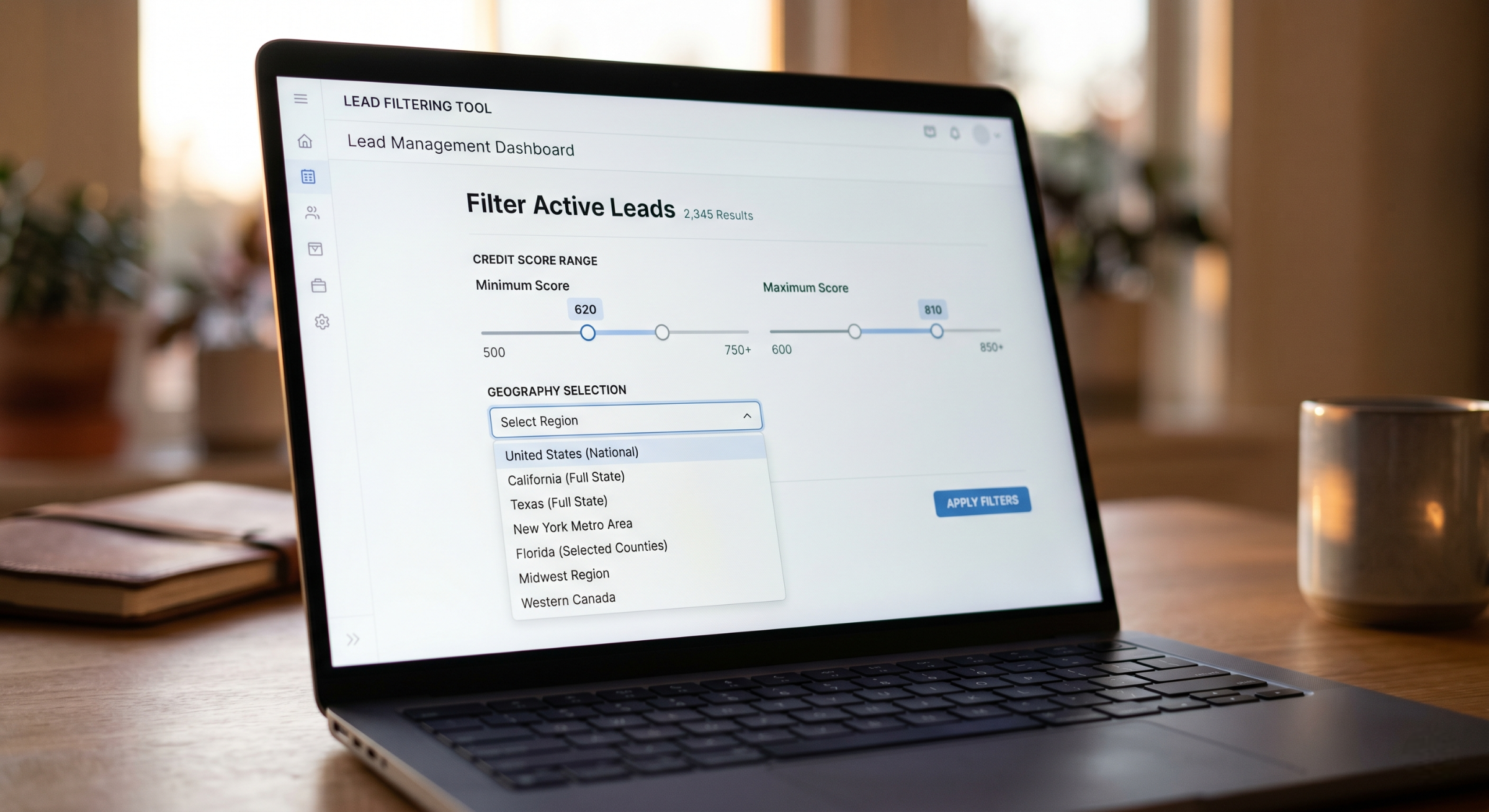

Filtering by Credit Score

Credit score filtering lets you receive leads that match the type of financing your dealership or lending product is set up to handle.

Here’s why that matters in practice.

If your financing products are designed for standard credit buyers, sending your team after subprime leads means a lot of declined applications and frustrated conversations. If you specialize in subprime, standard credit leads are likely to find better terms elsewhere and you’ve spent time and money on a buyer you can’t actually serve well.

Matching the lead to your product makes the first conversation more productive for everyone involved.

How credit score filtering typically works

Most lead providers let you set a credit range when you place your order. Common brackets look something like this.

Super prime buyers tend to sit above 720. Prime buyers generally fall between 660 and 720. Near prime runs from roughly 600 to 660. Subprime sits below 600.

The exact brackets vary by provider. What matters is that you know which range your financing products serve best and that you’re buying leads within that range rather than across the board.

What to ask your lead provider

Before you commit to a credit-filtered lead package, get clear on a few things. How is the credit range determined? Is it based on a hard pull, a soft pull, or self-reported information from the buyer? Self-reported credit ranges are less reliable than verified data. A buyer who thinks they have good credit and a buyer who has had their credit verified are not the same lead.

Working with a lead provider that verifies credit range before delivery makes a meaningful difference to your conversion rate on filtered leads.