Subprime vs. Deep Subprime Auto Leads: Key Differences

Autocarleads | Updated April 2026 | 7 min read

Subprime is a broad category and treating it as a single uniform buyer profile is one of the more common mistakes dealerships make when building their subprime finance operation.

Understanding the difference between subprime and deep subprime auto leads before you build your lender routing and deal structure strategy is what separates dealerships that convert consistently in this market from the ones that wonder why their approval rate is lower than it should be.

The buyers are different. The lenders are different. The deal structure requirements are different. And the follow-up approach that works for one doesn’t always work for the other.

Where the Line Falls

The industry doesn’t use a single universal definition for where subprime ends and deep subprime begins. But the most widely used framework breaks it down like this.

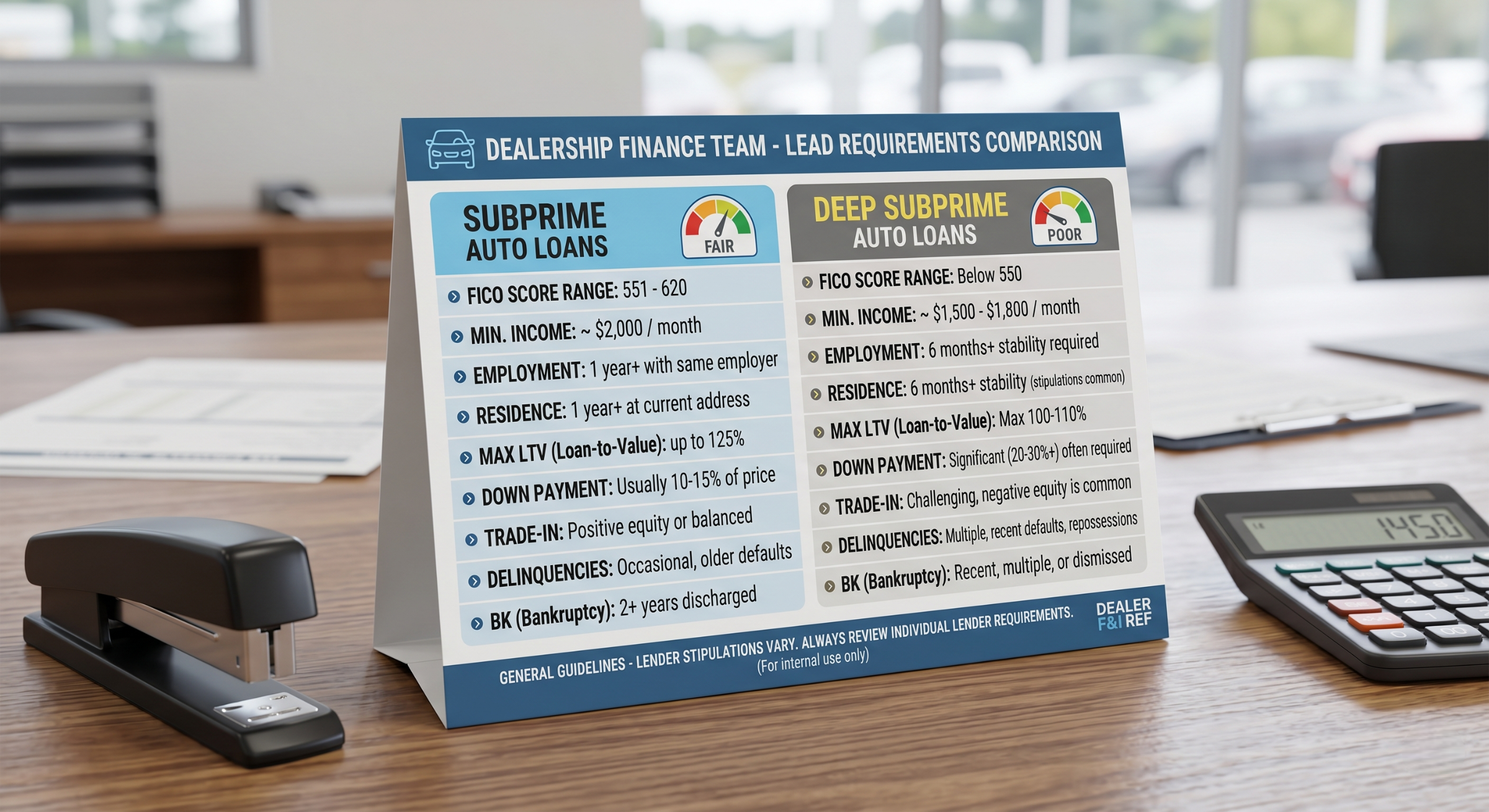

Subprime generally covers credit scores from roughly 501 to 600. These buyers have documented credit challenges but there’s typically something to work with in the file. Some positive history, some accounts in good standing, a credit story that a lender can evaluate even if parts of it aren’t clean.

Deep subprime covers scores at or below 500. The credit profile at this level is significantly more challenged. Multiple derogatory marks, collections, recent bankruptcies, or in some cases almost no credit history at all. The lender pool narrows considerably and the deal structure requirements tighten in response.

Near prime, the tier above subprime from roughly 601 to 640, is worth mentioning here because buyers near the boundary between near prime and subprime can sometimes be routed to standard channels depending on the lender. Understanding where all three tiers fall helps your finance team make faster, more accurate routing decisions.

How the Buyer Profiles Differ

The credit score difference isn’t just a number. It reflects meaningfully different buyer situations that affect how you approach the conversation and structure the deal.

Subprime buyers

Most subprime buyers have a credit history that includes some positive elements alongside the challenges. They may have had a period of financial difficulty, job loss, medical debt, or a specific event that damaged their score, but they’ve often maintained some accounts in reasonable standing.

Many subprime buyers have financed vehicles before. They understand roughly how the process works. They may have a sense of what rate range to expect even if they’re not sure exactly where they’ll land.

The income verification and employment stability requirements for this tier are meaningful but often workable. A buyer with a 570 score, two years at the same job, and a modest down payment available has a real path to approval through the right specialist lender.

Deep subprime buyers

Deep subprime buyers are dealing with more significant credit damage. Recent bankruptcies, multiple collection accounts, charge-offs, or a credit history that’s essentially absent are common. The lender is looking at a profile that offers very little traditional credit data to evaluate.

What takes over at this level is income verification and down payment. Lenders who work in deep subprime territory are essentially making an ability-to-pay determination rather than a creditworthiness determination. The question isn’t what the buyer’s track record looks like. It’s whether they have the income and the financial commitment, reflected in the down payment, to make the payment work.

Many deep subprime buyers haven’t financed a vehicle recently or have had a previous financing experience end poorly. The emotional context of the conversation is different. There’s often more uncertainty about whether approval is even possible and more sensitivity around how the conversation is handled.

How the Lender Landscape Differs

This is where the operational difference between the two tiers becomes most concrete.

Subprime lender options

The subprime tier from 501 to 600 has a reasonably developed lender market. Independent finance companies that specialize in challenged credit operate across this range. Some captive finance arms have products that reach into the upper end of the subprime tier. A dealership with two or three strong specialist lender relationships has real routing flexibility across most of the subprime range.

Approval rates in this tier, with appropriate deal structure and the right lender match, can be competitive with what a well-run prime operation achieves. The deals take more work but they close.

Deep subprime lender options

The lender pool at deep subprime is significantly smaller. Most independent finance companies have minimum score floors that fall somewhere between 480 and 520. Below those floors, buy here pay here is typically the most accessible path.

A small number of specialist lenders operate specifically in the deep subprime and no-credit segments. These relationships are worth developing if your dealership serves a market with significant deep subprime volume. They’re harder to find and typically come with more specific vehicle and deal structure requirements than standard subprime lenders.

For deep subprime buyers who don’t fit any external lender’s criteria, buy here pay here is the safety net that keeps the deal alive. The terms are the least favorable available but the approval flexibility is unmatched.

Deal Structure Differences

The structural requirements of a deal change meaningfully as you move from subprime into deep subprime territory.

Down payment requirements

Subprime lenders typically require somewhere between $500 and $1,500 as a minimum down payment. Some are flexible on this for buyers with stronger compensating factors elsewhere in the application. A buyer at 580 with solid employment history and low existing debt may get approved with a modest down payment through the right lender.

Deep subprime lenders require more. Minimums of $1,500 to $3,000 are common. Some require 20 percent or more of the vehicle price upfront. The down payment is serving a dual purpose at this level. It reduces the lender’s LTV exposure and it signals that the buyer is genuinely committed to the transaction. A buyer who can’t meet the down payment requirement at deep subprime usually doesn’t have a path to approval through standard financing channels.

Vehicle selection

Both tiers benefit from keeping the vehicle in a reasonable price and age range but the constraints are tighter at deep subprime.

Subprime lenders are typically comfortable with vehicles up to 10 years old with up to 100,000 to 120,000 miles in the $8,000 to $20,000 range. The specific parameters vary by lender but there’s reasonable flexibility.

Deep subprime lenders tend to want newer vehicles with lower mileage because predictable collateral value is more important when the credit profile is more uncertain. Some deep subprime programs are limited to vehicles below a certain age or within a specific price ceiling. Knowing your lender’s vehicle requirements before you start showing inventory saves time and manages expectations.

Loan-to-value requirements

Subprime lenders typically work up to LTVs of around 110 to 120 percent. This allows some flexibility on pricing without requiring the buyer to cover the full gap between the price and book value with a down payment.

Deep subprime lenders often want to stay closer to 100 percent LTV or even below it. At this level, the lender wants the collateral to fully cover the loan amount because the credit profile doesn’t offer the additional security that a stronger credit history would. Deals structured above the lender’s LTV threshold in this tier rarely get approved regardless of other compensating factors.

How the Follow-Up Approach Differs

Both tiers require more consultative follow-up than standard credit leads. But the specific approach differs in ways worth understanding.

Subprime follow-up

Subprime buyers often need help understanding what’s possible given their credit situation. The first call is partly information gathering and partly expectation setting. What vehicle range makes sense? Do they have a down payment? Are they aware their rate will be higher than standard?

A structured multi-touch follow-up over 48 to 72 hours works well for most subprime leads. These buyers are generally reachable and have enough familiarity with the financing process to engage in a productive conversation once you connect.

Deep subprime follow-up

Deep subprime buyers sometimes need more time and more touches before they’re ready to have a productive conversation about financing. The uncertainty about whether approval is possible at all can make buyers hesitant to engage until they feel confident the dealership is genuinely trying to help rather than going through motions.

Patience and consistency matter more in this tier. A buyer who doesn’t respond to the first two or three contacts may respond on the fourth or fifth when the repeated outreach signals that you’re serious about helping them find a path forward. That patience is part of what converts deep subprime leads at a meaningful rate.

The language in the follow-up matters too. Framing the conversation around finding a solution rather than qualifying the buyer for a specific product creates a different dynamic than a standard sales follow-up approach.

Lead Quality Considerations by Tier

The quality standards that matter for any auto lead apply to both tiers but with some tier-specific nuances.

For subprime leads

Intent verification, contact validation, and geographic matching are the core quality indicators. A subprime lead from a buyer who actively searched for bad credit auto financing, filled out a specific inquiry, and lives within your service area is a lead worth working aggressively.

Credit range accuracy matters here too. A lead classified as subprime based on verified data rather than self-reporting is a more reliable match for your subprime lender relationships. Self-reported credit ranges in this tier are often off in ways that create routing confusion.

For deep subprime leads

Everything above applies and income verification signals become more important. A deep subprime lead that includes income information alongside the contact details gives your finance team more to work with before the first call.

Geographic matching is particularly important at this tier because the lender pool is smaller and some specialist deep subprime lenders operate only in specific states or regions. A deep subprime lead from outside your lender’s geographic coverage isn’t a lead you can do much with regardless of the buyer’s other characteristics.

Buying subprime and deep subprime auto leads with verified credit range data is the most reliable way to ensure the leads you receive actually match the lender relationships you’ve built for each tier.

Tracking Performance Separately by Tier

This is worth emphasizing because it’s one of the habits that most consistently separates strong subprime operations from average ones.

Track contact rate, conversion rate, and cost per closed deal separately for subprime and deep subprime. The performance difference between the two tiers tells you where your lender relationships and deal structure capabilities are strongest and where there are gaps worth addressing.

A dealership converting subprime at 14 percent and deep subprime at 5 percent has a deep subprime process or lender relationship problem worth diagnosing specifically. Blending the numbers hides that signal and makes it impossible to address the right issue.

Tracking auto loan lead performance separately by subprime tier is the operational habit that turns credit tier awareness into actionable improvements.

The Bottom Line

Subprime and deep subprime are not the same market served by the same approach.

The buyers are different, the lenders are different, the deal structure requirements are different, and the follow-up that converts in one tier doesn’t automatically transfer to the other. Treating them as a single category produces blended results that obscure what’s actually working and what isn’t.

Build your lender relationships, your deal structure approach, and your follow-up process with the specific differences between these tiers in mind. The dealerships that do this consistently outperform the ones treating all challenged credit as a single undifferentiated challenge.

How Autocarleads Segments Subprime and Deep Subprime Leads

Every lead that comes through Autocarleads includes credit range classification based on verified data. Subprime and deep subprime leads are segmented accurately so your team knows what tier they’re working with before the first call and can route to the right lender from the start.

Real-time delivery, validated contact information, and geographic matching that reflects your actual service area.

See what subprime and deep subprime lead options are available in your market.

Frequently Asked Questions

Can the same lender handle both subprime and deep subprime applications?

Some can but most have distinct products for each tier with different approval criteria and rate structures. A lender who handles subprime well may have a floor around 520 or 540 that puts deep subprime buyers outside their appetite entirely. Knowing where each of your lender relationships draws its floor is the routing knowledge that prevents wasted submissions and unnecessary hard inquiries.

Is deep subprime worth pursuing if buy here pay here is the primary lender option?

It depends on your business model and your market. Dealerships with strong buy here pay here operations can build a profitable deep subprime business around that model. The margins are structured differently from financed deals and the operational requirements are specific. For dealerships without a buy here pay here structure, deep subprime volume is more limited to the buyers who qualify through the small number of specialist external lenders in this tier.

How do compensating factors differ between subprime and deep subprime underwriting?

In the subprime range, a combination of employment stability, modest down payment, and reasonable debt-to-income ratio can compensate meaningfully for a lower credit score. In deep subprime, the weighting shifts heavily toward income verification and down payment because there’s less credit history to evaluate alongside those factors. A deep subprime buyer with strong income and a significant down payment has a real path to approval through the right lender. One without those compensating factors typically doesn’t.

Should I buy subprime and deep subprime leads from the same provider?

It’s workable if the provider accurately segments both tiers based on verified data. The risk is that providers who use self-reported credit ranges produce inaccurate tier classifications that mix the two buyer profiles in ways that create routing confusion. Confirmed verified data from a single provider who handles both tiers accurately is preferable to using two separate providers for the sake of segmentation alone.

What's the realistic conversion rate difference between subprime and deep subprime leads?

A well-run operation typically sees deep subprime convert at 40 to 60 percent of the rate achieved in standard subprime. If subprime is converting at 14 percent, deep subprime converting at 6 to 8 percent is a realistic range for a dealership with appropriate lender relationships and deal structure capability for that tier. The lower conversion rate reflects the smaller lender pool and more specific deal requirements rather than buyer intent. Deep subprime buyers who find a lender willing to approve them are often among the most committed customers in the dealership.