What to Look for in a Subprime Lender Relationship

Not all lenders who claim to work in the subprime space deliver what that claim suggests. Here’s how to evaluate any lender relationship before you commit to routing volume through it.

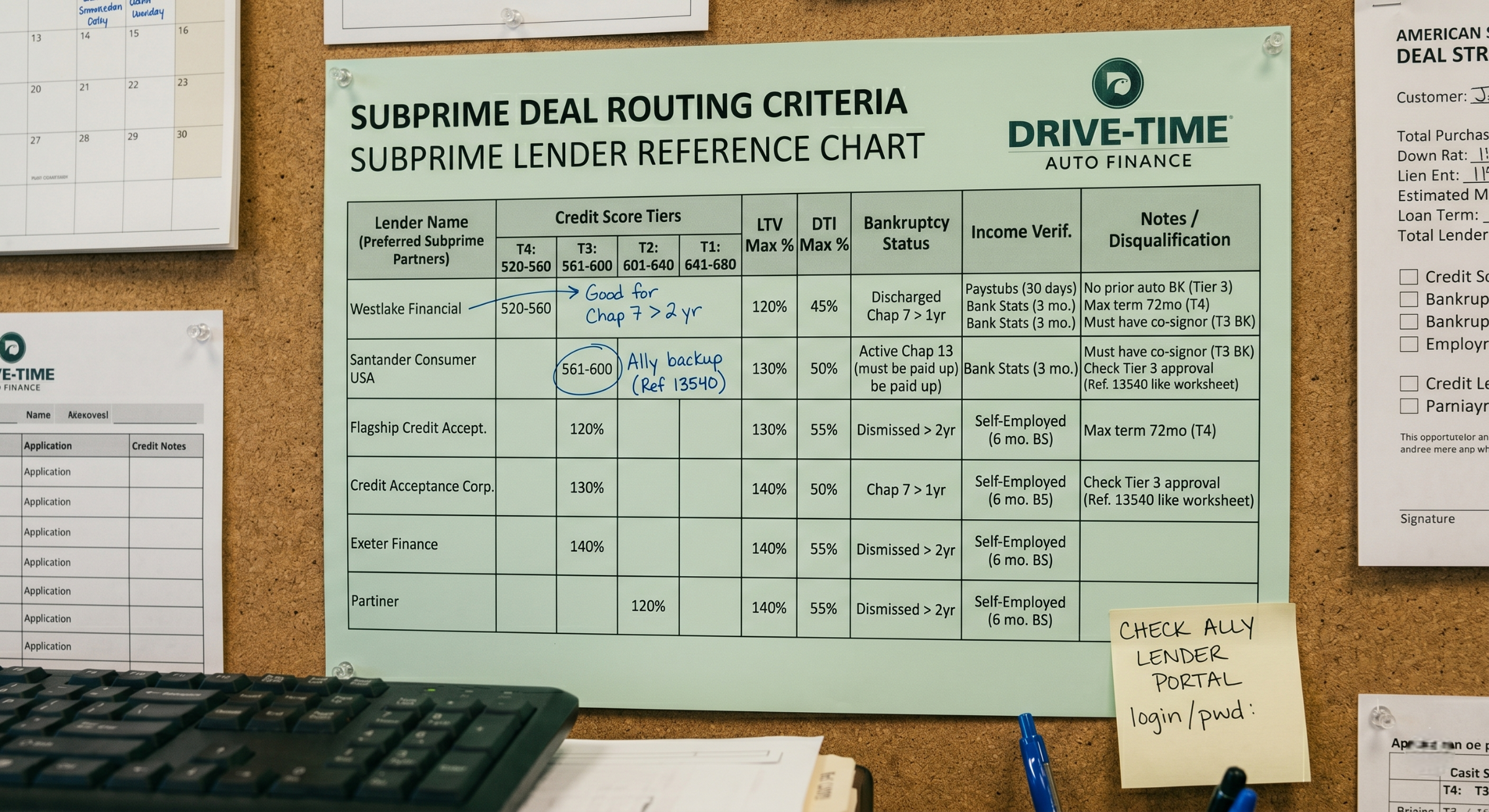

Clear, published credit tier criteria

A lender worth working with has specific, documented criteria for what they’ll approve. Minimum score, maximum score, down payment requirements at different tiers, vehicle restrictions, LTV limits, payment-to-income ceiling. This information should be available to their dealer partners clearly and without requiring a call to find out every time.

Lenders who are vague about their criteria create routing guesswork that produces unnecessary declines. Routing accuracy requires specific information and a lender who won’t provide it specifically is telling you something about how the relationship will work.

Competitive rates for the tier they serve

Rates vary between subprime lenders even for similar credit profiles. A lender whose rates are consistently at the high end of the market relative to competitors in the same tier may be creating a buyer experience problem. Buyers who accept a high rate because they feel they have no options are less satisfied customers and sometimes don’t complete the loan when a better option surfaces.

Knowing where your lenders’ rates sit relative to the market helps you route with the buyer’s experience in mind rather than purely based on approval likelihood.

Reasonable approval turnaround

Subprime buyers are often in a more fragile decision state than prime buyers. An approval that takes three days to come back gives a buyer time to reconsider, find another option, or simply disengage from the process. Lenders who consistently turn around decisions quickly, same day or next day, are significantly more useful in a subprime operation than those who take longer.

Ask about typical approval turnaround during the relationship development conversation and follow up on actual experience once you start routing volume.

Responsive dealer support

Problems arise in subprime financing more frequently than in standard financing because the deals are more complex. A lender with responsive dealer support, a specific contact who knows your operation and responds quickly when something needs resolution, is worth considerably more than a lender with a general customer service queue that treats every dealer inquiry the same.

The quality of dealer support often only becomes apparent after a problem surfaces. Building relationships with lenders whose reputation for dealer support is strong before you need it is better than finding out it’s poor at the worst possible moment.

Consistent standards over time

Some lenders tighten or loosen their credit criteria frequently in response to portfolio performance or market conditions. A lender who changes their minimum score, their down payment requirements, or their vehicle restrictions without clear communication to dealer partners creates operational problems.

Lenders who maintain consistent standards and communicate changes clearly are easier to work with over the long term than those who shift criteria frequently. Longevity of the relationship and stability of the criteria go together.